The Final State of the Union

Last week, President Obama laid out a plan to help responsible homeowners who were struck by the housing crisis. Atop the proposed “Homeowner Bill of Rights” is a pledge to simplify mortgage disclosure forms. Thankfully, inspired by the principles of running a “lean startup”, the Consumer Financial Protection Bureau tapped into the expertise of the American people through the “Know Before You Owe” initiative.

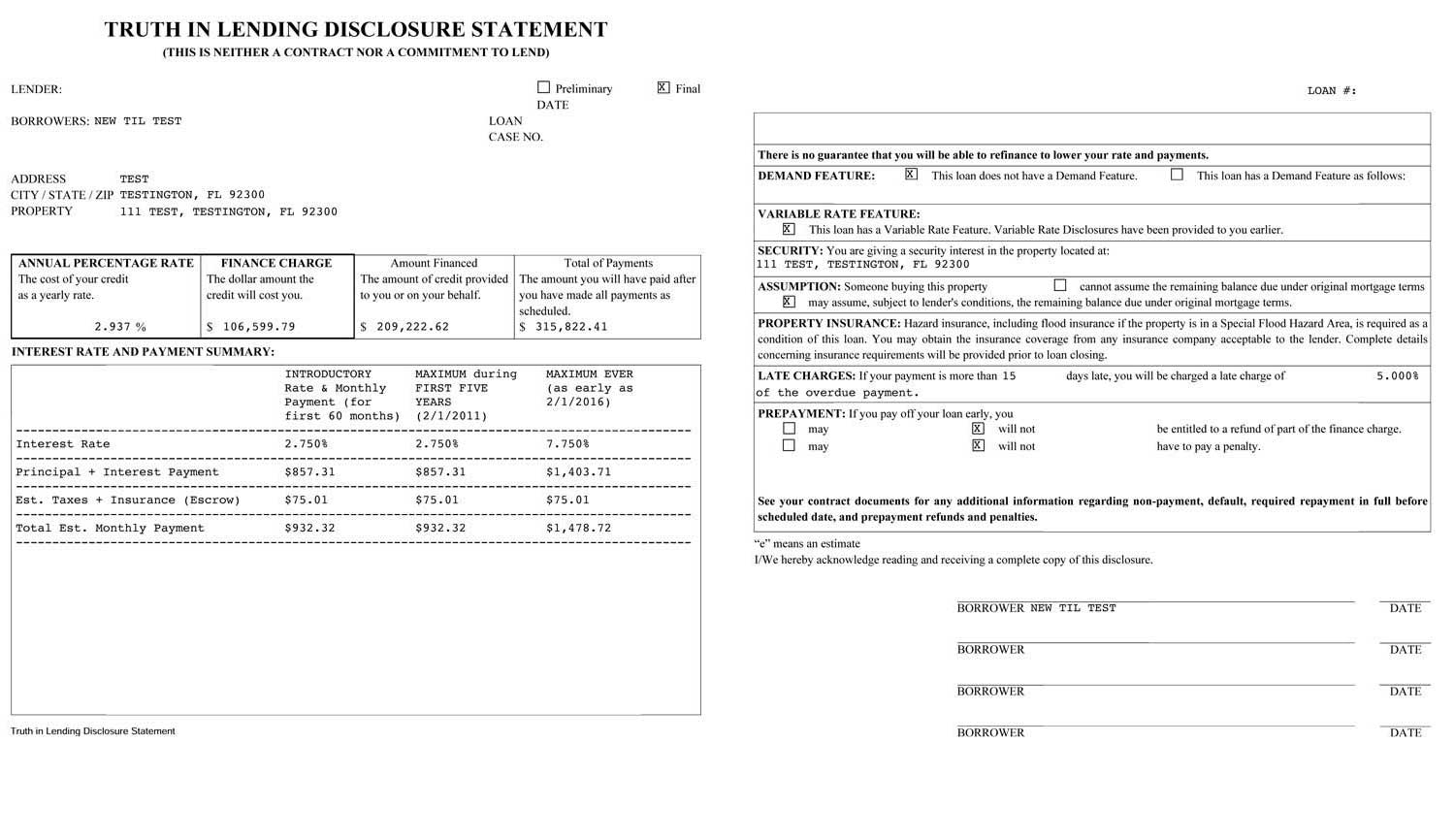

As background, everyone who applies for a mortgage loan receives two federally mandated disclosures with information about the mortgage: the Truth in Lending form and the Good Faith Estimate. The Dodd-Frank Act required the CFPB to combine these two forms into a single simplified disclosure. Empowering consumers with information is only as helpful as the design that ensures the data helps them make purchase decisions. Thus, the Bureau focused on making the new combined disclosure clear to consumers and lenders alike.

“Know Before You Owe” launched last May with two draft designs accessible online with an explicit call for public participation. The CFPB built tools to help make sense of the data, and complemented it with in-person testing to inform future versions. They leveraged heatmaps to capture the areas on each form that received the most attention; synthesized more than 13,000 user comments; and analyzed where participation was most prevalent.

The Know Before You Owe mortgage disclosure testing is now in its ninth iteration and will wrap up next month. The project has expanded to include both the application disclosures and the disclosures consumers receive when they finalize their mortgages. In the spirit of “lean startups” the Bureau has refined the forms with each participatory session. For example:

Soon, the Bureau will write a rule to create the new disclosures. The people writing the rule will have tens of thousands of comments from consumers and the mortgage lending industry to help them understand what is effective and what is not. Consumers in the future will have a clearer picture of what they owe before they owe it because consumers today have helped design the disclosures they’ll receive. Lenders in the future will have an easier time complying with disclosure laws and communicating with borrowers because lenders today have helped design the disclosures they’ll use.

Iterating against user feedback and using technology to open the design process has been part of a broad collaborative approach at the CFPB. It has been so successful that the CFPB has expanded the idea to college financial aid letters and credit card agreements, as well.

Thanks for your participation.

Aneesh Chopra is U.S. Chief Technology Officer

{kind=link}