The Final State of the Union

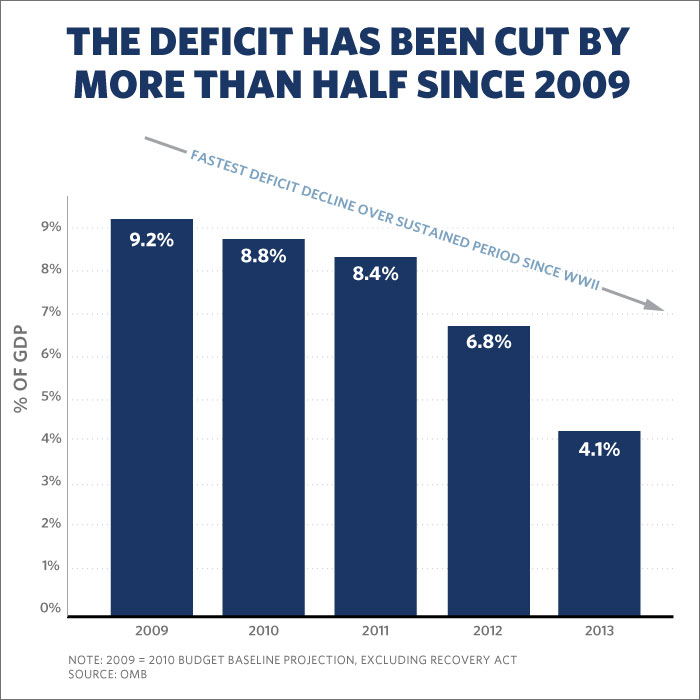

The Office of Management and Budget and the Department of the Treasury today released the fiscal year (FY) 2013 budget results, which show that we are continuing to make significant progress in reducing the deficit. The final 2013 deficit was $680 billion, $409 billion less than the 2012 deficit and $293 billion less than forecast in President Obama’s April Budget. As a percent of Gross Domestic Product (GDP), the deficit fell to 4.1 percent, representing a reduction of more than half from the deficit that the Administration inherited when the President took office in 2009. The deficit reduction since that point represents the fastest decline in the deficit over a sustained period since the end of World War II.

The President believes that growing our economy and creating more good jobs with higher wages must be our top economic priority. That is why he has consistently advocated a strategy to strengthen the middle class while improving our nation’s long-term fiscal position by cutting the deficit in a balanced way. Under the President's leadership, we have already locked in more than $2.5 trillion of deficit reduction over the next decade, through a combination of spending cuts and revenue increases from asking the wealthiest to pay their share.

In his 2014 Budget, the President presented a plan that would make critical investments to strengthen the middle class, create jobs, and grow the economy, while continuing to cut the deficit in a balanced way. It is a plan that demonstrates that we do not need to choose between growing the economy and taking further action to reduce the deficit – we can do both. Building on the $2.5 trillion in deficit reduction already locked in, the President’s plan would replace the economically damaging sequester while achieving additional deficit reduction to put Federal debt on a downward path as a share of the economy. And unlike sequestration, which includes no long-term deficit reduction, the President’s plan includes structural reforms that would generate growing savings in the second decade and beyond.

The significant decrease in the deficit from last year was due to a combination of higher receipts and lower outlays in 2013, which can be attributed to a variety of factors, including a stronger economy, the expiration of certain tax cuts for high income Americans, and spending reductions like those achieved from the troop drawdown in Afghanistan as proposed in the President’s Budget.

Looking forward, the Administration remains committed to working with Congress to enact proposals that will strengthen the economy and middle class by making needed investments in areas like education, infrastructure, research and development, and national security, while putting debt as a share of the economy on a downward path.

Sylvia Mathews Burwell is the Director of the Office of Management and Budget.