The Final State of the Union

This morning, the Council of Economic Advisers is releasing the 2014 Economic Report of the President, which discusses the progress that has been made in recovering from the worst recession since the Great Depression, and President Obama’s agenda to build on this progress by creating jobs and expanding economic opportunity. This year’s report highlights steps the Obama Administration is taking to address three key imperatives: continuing to restore the economy to its full potential, expanding the economy’s potential over the long-run, and ensuring that all Americans have the opportunity to realize their full individual potential.

Below are seven highlights from each of the seven chapters in this year’s Report:

Chapter 1 introduces the Report and highlights several key areas where progress has been made, but it also lays out the areas where much more work remains to be done. In particular, recoveries from financial crises are uniquely challenging because heavy household debt burdens and tight credit conditions can linger for years, depressing spending and investment. However, as shown in Figure 1-4 of the Report, among the 12 countries that experienced a systemic financial crisis in 2007 and 2008, the United States is one of just two in which output per working-age person has returned to pre-crisis levels. The fact that the United States has been one of the best performing economies in the wake of the crisis supports the view that the full set of policy responses in the United States made a major difference in averting a substantially worse outcome—although it in no way changes the fact that more work remains to be done.

Chapter 2 reviews the economy’s performance in 2013 and discusses the key reasons why the Administration, like other forecasters, expects growth to strengthen in the coming years. Five years removed from the worst of the financial crisis, the economy continues to strengthen and recover, with businesses adding 2.4 million jobs in 2013, the third straight year private employment has risen by more than 2 million. Looking to 2014, one key reason that growth is expected to pick up is that households have made substantial progress in paying off debt, a process known as deleveraging, putting them in a better position to increase spending going forward. As shown in Figure 2-7, household debt has fallen from a peak of about 1.4 times annual disposable income in the fourth quarter of 2007 to 1.1 times annual disposable income by the fourth quarter of 2013. Similarly, debt service (that is, required minimum payments on household debt) has fallen from a high of 13 percent of disposable income in the fourth quarter of 2007 to 10 percent by the third quarter of 2013, its lowest since the data begin in 1980. It is important to note, however, that while these figures paint a picture of improvement in the aggregate, many moderate- and middle-income households have seen little benefit from recent stock market gains and are still grappling with the implications of home prices that, despite recent progress, remain well below their previous highs. Other reasons to expect stronger growth in 2014 than in 2013 include diminished fiscal drag, a recovery in asset values, strengthening among our international trading partners, and demographic forces that are expected to maintain upward pressure on housing starts—although all of these factors need to be balanced against the uncertain risks that can always adversely affect the economy.

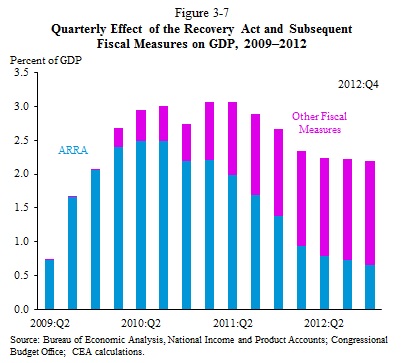

Chapter 3 evaluates the impact of the Recovery Act and subsequent fiscal jobs measures on the economy, finding that they made a substantial and sustained contribution to the level of jobs and output. CEA estimates that Recovery Act alone raised the level of GDP by between 2 and 2.5 percent from late 2009 through mid-2011. This estimate is also within the range of estimates provided by the Congressional Budget Office (CBO) and private-sector forecasters. But the efforts did not stop with the Recovery Act, and in the subsequent years the President signed more than a dozen additional fiscal measures to create jobs and strengthen the economy, including the payroll tax cut, small business tax cuts, incentives for infrastructure, and extended unemployment insurance. Combining the effects of the Recovery Act and the additional fiscal measures that followed, the cumulative boost to GDP from 2009 through 2012 is equivalent to 9.5 percent of fourth quarter 2008 GDP (Figure 3-7). In addition to discussing the immediate macroeconomic impact, Chapter 3 also explains how the Recovery Act kept millions of families out of poverty and made investments in clean energy, education, and infrastructure that will continue to pay dividends long after the Act has phased out.

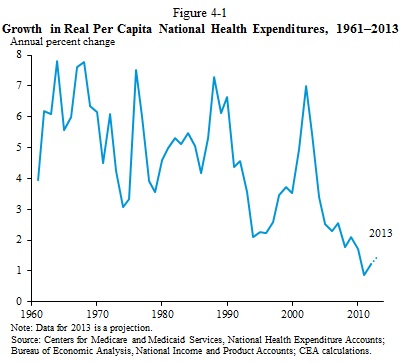

Chapter 4 analyzes the causes and consequences of the historic slowdown in the growth of health care costs, which has potentially massive implications for families, employers, and the Federal budget. The growth rate of real per-capita health care expenditures from 2010 to 2012 was the lowest since data collection began in the 1960s, and preliminary data and projections indicate that slow growth continued into 2013 (Figure 4-1). It does not appear that this development is merely an after-effect of the recession, as the slowdown has now persisted well into the economic recovery. Chapter 4 analyzes a variety of factors behind the slowdown, including the Affordable Care Act, which is contributing to this trend by reducing excessive payments to Medicare providers and private insurers, as well as by deploying payment reforms that incentivize more efficient, higher-quality care. This slowdown will help raise incomes, act as a tailwind for job creation and growth, and contribute to deficit reduction.

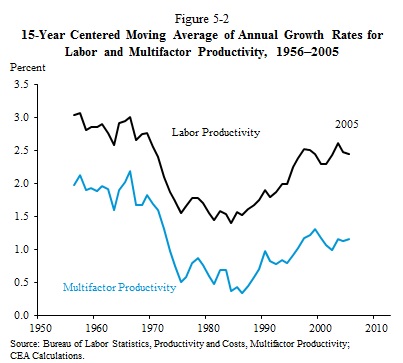

Chapter 5 discusses the vast advances that have been made in the technology sector in recent years, the broader context of productivity growth over the last 60 years, and the President’s agenda to support research and foster innovation going forward. Figure 5-2 shows that over the last two decades, productivity has grown faster than in the 1970s and 1980s, but more slowly than in the 1950s and 1960s, when rapid productivity growth was fueled by public investments like the interstate highway system and the commercialization of innovations from World War II like the jet engine and synthetic rubber. Recent technological advances have unleashed a great deal of potential, and Chapter 5 discusses steps the Obama Administration is taking to support innovation, in particular expanding the availability and efficiency of wireless spectrum for commercial broadband use and reforming the patent system to ensure that it encourages useful innovation by inventors and limits wasteful litigation by patent assertion entities, also known as “patent trolls.”

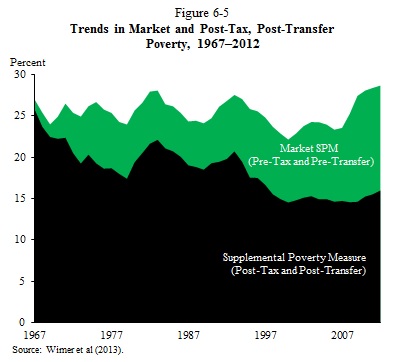

Chapter 6 takes stock of the progress that has been made, lessons that have been learned, and ways to take the next step forward in combating poverty 50 years after the start of the War on Poverty. Using new historical estimates of poverty based on modern measurement methods, Chapter 6 presents a more accurate picture of the changes in poverty over the past five decades. Since 1967, the first year for which such estimates are available, the poverty rate has fallen by nearly 40 percent. Crucially, all of this reduction in poverty has come as a result of tax credits and government programs such as Social Security, nutrition assistance, unemployment insurance, among others. Over this time period, expansions in tax credits that support working families have led the Earned Income Tax Credit (EITC) and the refundable Child Tax Credit (CTC) to lift more children out of poverty than any other Federal program. Expansions of the EITC and the refundable CTC enacted during this Administration benefit 16 million families with 30 million children and have helped keep about 1.4 million Americans out of poverty. Altogether, the EITC and the refundable CTC now support 32 million working families, lifting 10.1 million people, including 5.3 million children, out of poverty. Excluding the effects of these programs, poverty would be slightly higher than it was in 1967. Drawing on this crucial insight, Chapter 6 lays out ways that safety net programs can be strengthened, as well as ways to take the next step forward in fighting poverty by raising wages, thereby increasing incomes before government programs kick in. Specifically, the President has called for measures like an expansion of the Earned Income Tax Credit for households without children and an increase in the minimum wage that would raise incomes for tens of millions while alleviating poverty for millions.

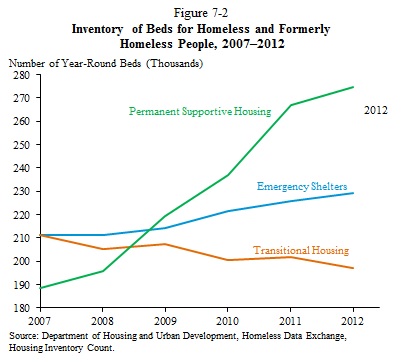

Chapter 7 focuses on how high-quality “impact” evaluations of Federal programs can influence public policy for the better, and how they have been used to focus Federal dollars on strategies that work. Figure 7-2 provides a telling example: sharply reducing homelessness is a key Administration focus, and based on evidence from program evaluations, the Department of Housing and Urban Development has re-oriented the Homelessness Assistance Grant Program away from traditional approaches such as transitional housing toward more effective permanent supportive housing. Rigorous impact evaluations such as these have long been supported by the President. In his 21st Century Management Agenda, the President set bold goals for building a more efficient, more effective government—one which contributes to economic growth and strengthens the foundations for economic prosperity. More work remains to be done however, and Chapter 7 describes opportunities for further progress in building actionable evidence to answer important program and policy questions.