The Final State of the Union

The level of long-term interest rates is of central importance in the macroeconomy. It matters to borrowers looking to start a business or buy a home; lenders evaluating the risk and rewards of extending credit; savers preparing for college or retirement; and policymakers crafting the government’s budget.

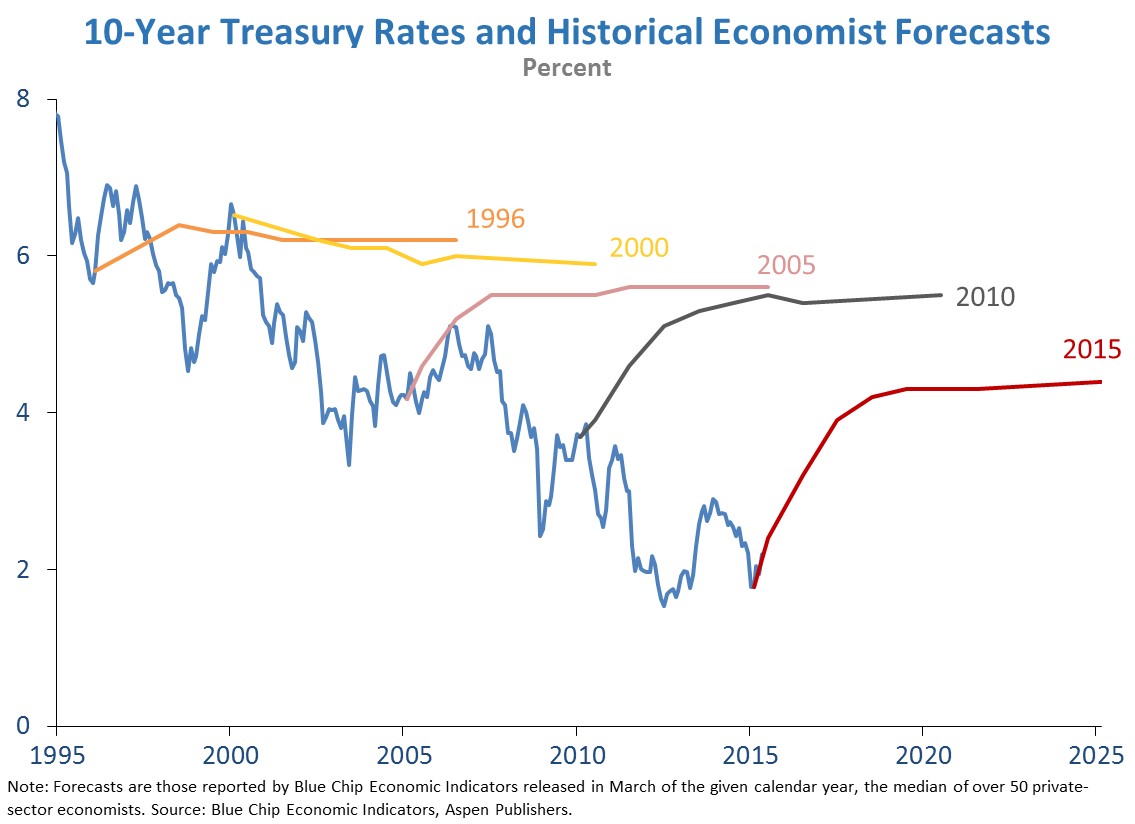

Long-term interest rates in the United States have been falling since the early 1980s and have reached historically low levels. But does this experience indicate that the level of long-term interest rates has shifted to a lower long-run equilibrium? A new report by the Council of Economic Advisers surveys the latest thinking on the many drivers of interest rates, both in recent decades and into the future. While there is no definitive answer to the question, most explanations for currently low long-term interest rates suggest that in the long run, they will remain lower relative to those that prevailed before the financial crisis.

The decline in interest rates over the last three decades has at least three notable characteristics:

The natural question – "Are long-term interest rates likely to stabilize at levels permanently below those that prevailed before the financial crisis?" – is an important one for policymakers and private-sector decision makers alike, yet economic analysts disagree on the answer.

A recent debate between two eminent economists and former policymakers, Ben Bernanke and Larry Summers, epitomizes the disagreement. Drawing on his “global saving glut” theory, Bernanke sees world interest rates pushed down by excessive global saving that is largely the result of government policies such as foreign reserve accumulation. To the extent those polices are reversed, interest rates should rise. Summers, however, attributes low interest rates to chronically deficient demand, under a hypothesis called “secular stagnation.” This view argues that prolonged low interest rates are inevitable and will continue unless governments step in directly with policies to boost aggregate demand, such as higher infrastructure spending.

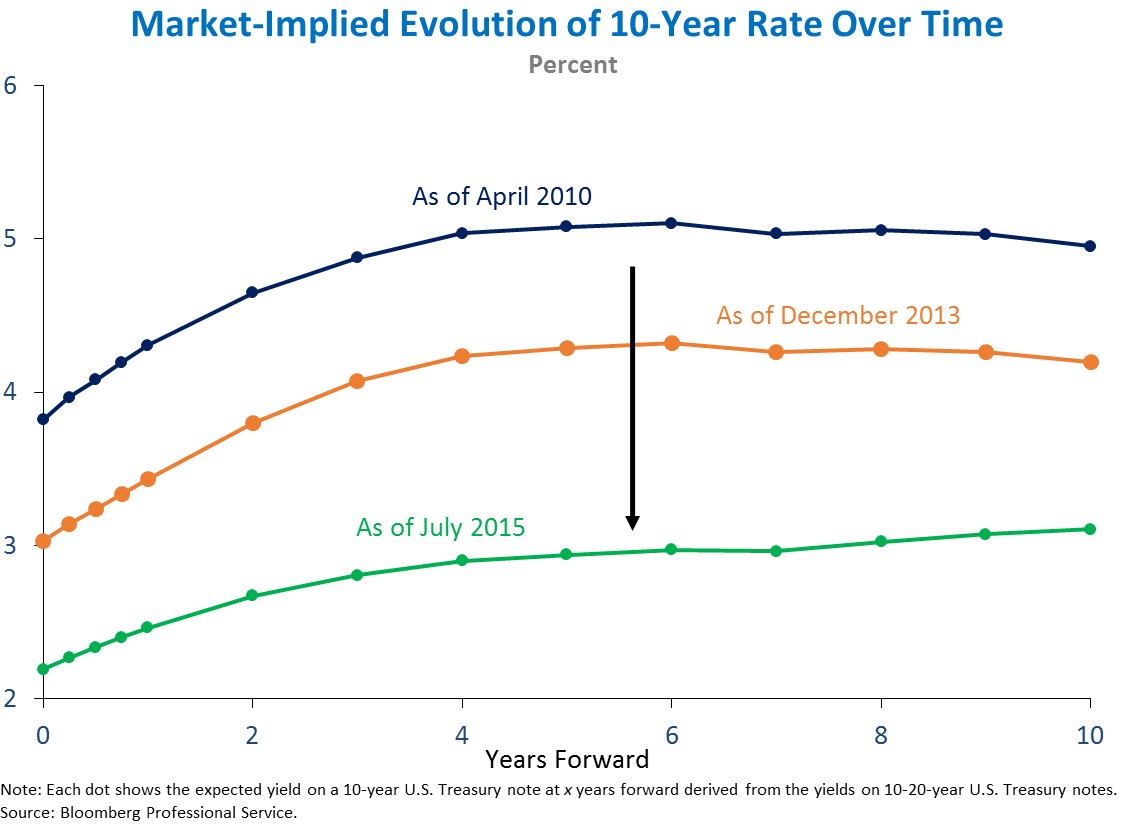

Prices of financial assets are based on expectations about the future. Traders in bond markets often perform “forward transactions” that involve selling and buying assets with different maturity lengths; such transactions can provide a proxy for expectations of future interest rates. For example, purchasing a 20-year Treasury bond, while simultaneously selling an asset that pays the first ten years of its coupon payments, approximates the purchase of a 10-year bond in 10 years. The net cost of that transaction yields a measure of the 10-year interest rate expected to prevail in ten years, called the forward rate.

As the figure below shows, the forward rate measure of the expected 10-year interest rate has declined sharply over time and currently stands at 3.1 percent, substantially below most professional forecasts.

The forward rate reflects the expected future interest rate as well as the term premium in the price of the 20-year bond used in the forward transaction. (The term premium is the extra compensation that investors receive for the risk of holding a long-term bond, which has a variable price.) Its dependence on the term premium, however, makes the forward rate an imperfect measure of the expected future interest rate. Nonetheless, the fact that the forward rate has declined roughly 180 basis points since 2010 is a striking development that is difficult to explain without a large concurrent fall in expected long-term interest rates. Professional forecasts of the long-term interest rate ten years from now also reflect an expectation that future rates will remain low.

An alternative way to think about whether the level of long-term interest rates has shifted to a lower long-run equilibrium is to examine the factors that have lowered rates today and assess which of them are likely to continue, although there is considerable uncertainty in undertaking this exercise.

Factors that Likely Are Transitory

Factors that Likely Are Longer-Lived

While some of the factors causing low long-term interest rates today will very likely dissipate over time, others have the potential to be much longer-lasting. There is no definitive answer to how long current low long-term interest rates will persist and whether they will settle at levels below those previously expected. Most factors, however, suggest that long-term interest rates will be lower in the long run compared with their levels before the financial crisis.

Maurice Obstfeld is a Member of the Council of Economic Advisers. Linda Tesar is a Senior Economist on the Council of Economic Advisers.