This is just one story of the millions of Americans whose lives have been changed by the Affordable Care Act. This kind of change has been a long time in the making.

After nearly 100 years of talk, and decades of trying, President Obama finally made affordable, quality health care for all a reality for America. Today, 20 million more adults have health insurance. Three million additional children have health insurance than in 2008. America's uninsured rate now stands at its lowest level ever. One hundred and five million Americans no longer have lifetime limits on their coverage and 137 million Americans now have a right to coverage for critical preventive services with no out-of-pocket costs, like flu shots, yearly check-ups for women, and birth control.

No matter who you are, chances are you're benefiting from an improved health care system thanks to the Affordable Care Act. You may not realize that there's a lot to lose if Republicans succeed in repealing this law. Here's a look at a few different scenarios that reflect the lives of many Americans, and what happens with and without this law in place.

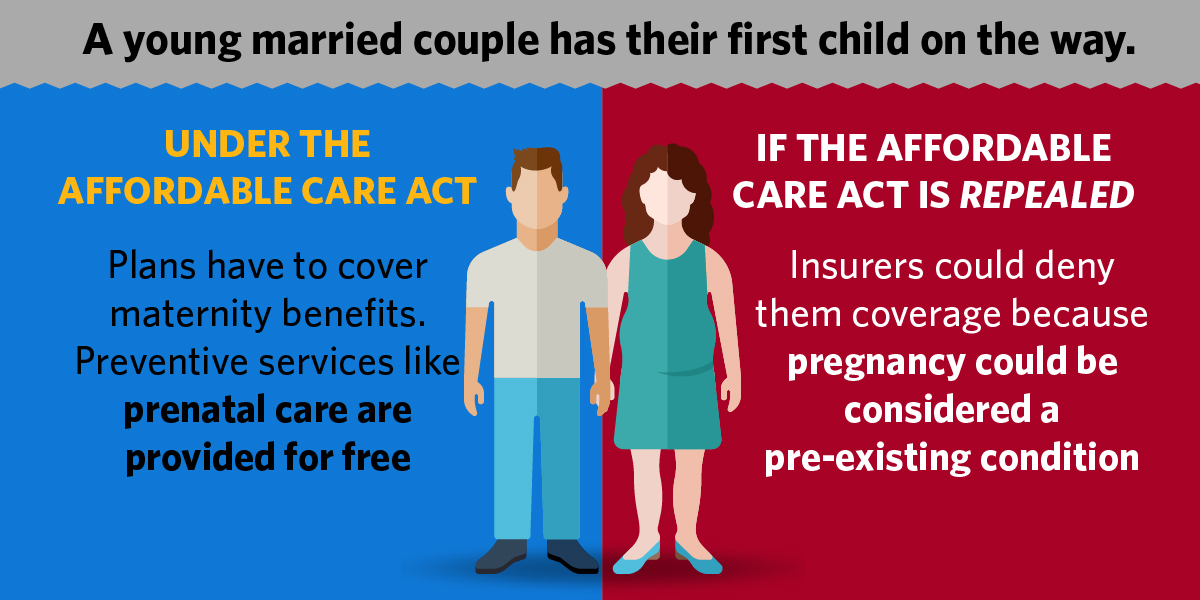

A young married couple receive news that they are going to have their first child, and decide to move closer to their family. Thanks to the Affordable Care Act (ACA) they can find health care coverage through the Marketplace even though their new jobs, which have a combined income of $40,000, do not provide coverage.

More on how the ACA helps:

-

They are able to easily go online and compare plans to find one that works for them. As a result of their move, they qualify for a special enrollment period, and can choose a plan that provides coverage right away.

-

What’s more, they receive financial assistance that provides over $4,250 a year to reduce their premiums, covering over 55 percent of the cost, as well as reduces their out-of-pocket costs.

-

Thanks to the consumer protections in the ACA, their plan covers maternity benefits. It also covers preventive services like prenatal care with no out-of-pocket costs.

-

She goes to a hospital that takes part in the voluntary ACA program that helps to prevent unnecessary early deliveries and maximize the health of the mom and baby. The family may also qualify for a home visit that provides best practices for new parents.

-

The baby’s immunizations and well child visit are covered with no out-of-pocket cost.

If the ACA were repealed:

-

Pregnancy could be considered a pre-existing condition, meaning when this family looked for new coverage after moving, insurers could deny them coverage or charge exorbitant rates.

-

Their plan would likely not include maternity coverage, as was the case for over 60 percent of enrollees in individual market plans in 2011.

-

They’d receive no financial assistance to help ensure they can find a good plan within their budget. They would receive no help in paying their out-of-pocket costs.

-

The programs that support healthy pregnancies, births, and newborns would no longer exist, putting the family at greater risk of health problems.

-

And the family would likely have to pay out of pocket for each visit and shot for their new baby, putting them further behind on other household payments.

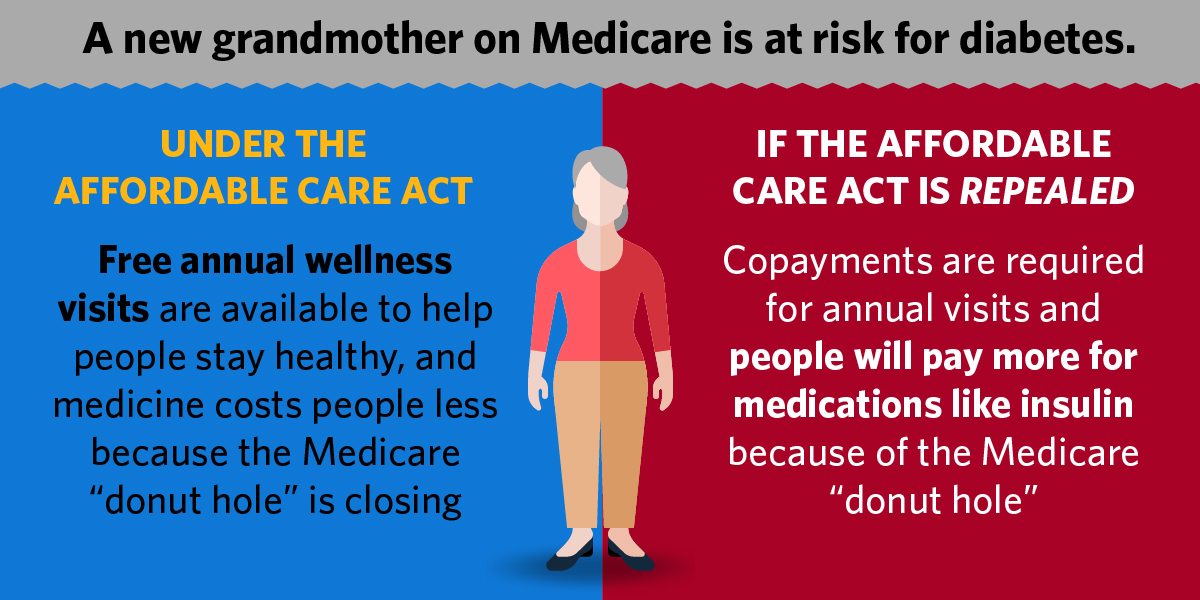

A Medicare beneficiary with pre-diabetes later develops diabetes, with significant associated costs and complications. She also suffers a fall and a subsequent hospitalization. The preventive services available through the ACA help her delay the onset of diabetes, and the ACA also helps to prevent further hospitalization and reduce medical problems. This allows the new grandmother to spend more time with her granddaughter.

More on how the ACA helps:

-

She can receive a free annual wellness visit, including a diabetes screening. Her doctor diagnoses her with pre-diabetes, meaning her blood sugar is high and she is at risk for developing diabetes in the future.

-

Her physician refers her to a Diabetes Prevention Program, which Medicare will start paying for nationwide. This Program suggests improvements in her diet and encourages her to increase her physical activity, helping her lose weight and reducing her chances of developing diabetes.

-

When she suffers a serious fall and is hospitalized, her hospital has improved patient safety practices as a result of the ACA, reducing the chance of her acquiring a potentially deadly infection during her stay.

-

Additionally, her hospital has improved its coordination with home health and other post-acute care providers, providing her with a smooth transition from the hospital back to her home, helping her recover more quickly and preventing a costly readmission to the hospital.

-

While preventive measures delay her development of diabetes, after five years, she does develop diabetes and requires insulin, which she gets through her Medicare Part D prescription drug plan. As a result of the ACA phasing out the Medicare “donut hole,” affected beneficiaries have saved an average of $2,127 on prescription drugs through July 2016, and her savings on these medications will increase annually until the “donut hole” is entirely closed in 2020.

If the ACA were repealed:

-

She would pay a copayment for her annual visit to her physician, which could cause her to skip the visit in order to save money.

-

As a result, she would not learn that she has pre-diabetes. Even if she were finally diagnosed with pre-diabetes, Medicare would not pay for the Diabetes Prevention Program, and thus she could quickly develop full-blown diabetes.

-

Because of the reopening of the Medicare “donut hole,” she would pay significantly more for her insulin and other medications, eating into her limited income and potentially causing her to skip doses in order to save money.

-

When she is finally discharged home after her fall, she would not have any assistance to help her understand her medications or how to contact the home health agency that will provide her follow up care. The unmanaged transition could lead her health to quickly deteriorate, resulting in a readmission to the hospital.

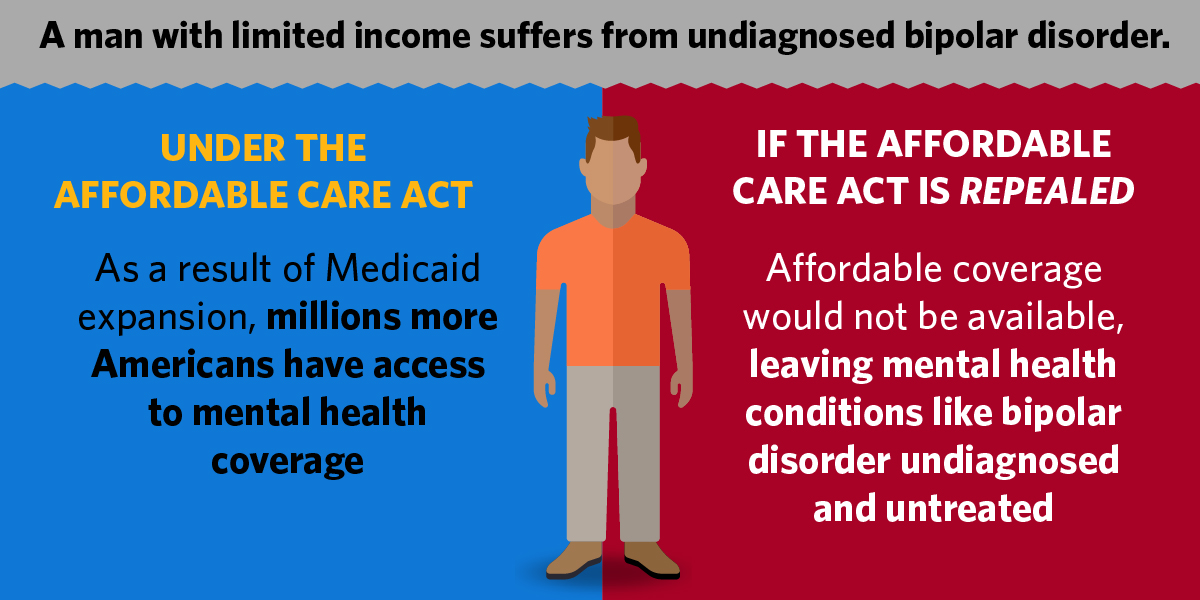

A man with a low income suffers from undiagnosed bipolar disorder. Thanks to the ACA, he has access to private insurance, despite his pre-existing condition, and to Medicaid in his state, and both have strong protections for enrollees with mental health challenges. Because his annual income is $12,000, he qualifies for Medicaid.

More on how the ACA helps:

-

Individuals with incomes up to 133 percent of the federal poverty level are now eligible for Medicaid expansion in States that choose to expand.

-

With coverage under his State’s Medicaid expansion, he is able to get the care and treatment he needs.

-

If his income rises by $5,000, he will qualify for private individual health insurance with financial assistance. For the first time, this man cannot be denied coverage based on a pre-existing mental health condition.

-

Individual market coverage must include mental health and substance use disorder services as an “essential health benefit” and the coverage must be generally comparable to the benefits offered for medical and surgical benefits.

If the ACA were repealed:

-

He would not afford coverage or doctor’s visits, and would have no regular source of primary care, so his condition would remain undiagnosed.

-

As a result of his lack of regular care, he would go to the emergency room frequently to receive care.

-

Lacking coverage, he would be unable to afford medication or to see a psychiatrist, which would cause his condition to worsen. Such circumstances often lead to substance use disorders.

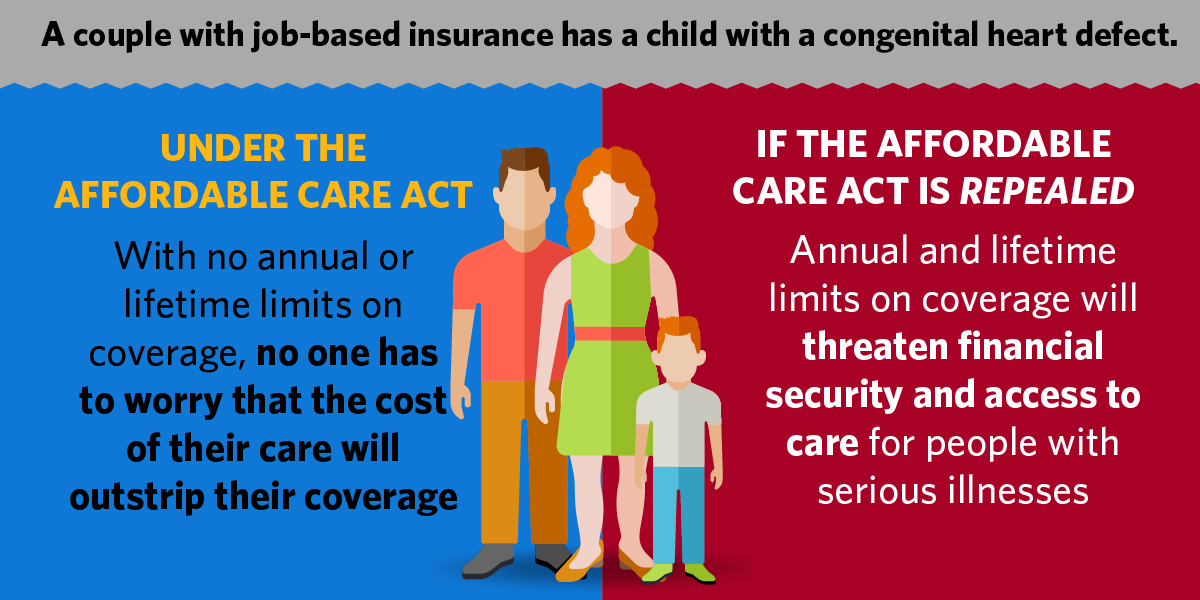

A couple with insurance through their employer gives birth to their second child, who is born with a congenital heart defect. Because of the complexity of the defect, the child requires immediate specialized care and will continue to need special heart care throughout his life. The ACA helps this family by preventing them from reaching an annual or lifetime limit on what insurance will cover. And, this child will always be insurable even though he has a pre-existing condition.

More on how the ACA helps:

-

There is no annual or lifetime dollar limit on the couple’s insurance plan. This means that they will not have to worry about medical bankruptcy because of the high cost of their son’s care. Prior to the ACA, 105 million people with employer plans had lifetime limits on their coverage, encompassing 59 percent of all workers covered by their employer’s health plan.

-

Their employer-provided plan also must now cap the out-of-pocket costs they can pay, and since the ACA became law an additional 22 million people have gained protection against catastrophic costs.

-

In addition, the ACA allows them to keep their son on their plan until he is 26, so they do not have to worry about how he will obtain coverage in the future, which was a serious problem for many young adults. Prior to the ACA, one in three young adults between the ages of 19 and 25 were uninsured.

-

And, because of the ACA’s ban on insurer discrimination against individual’s with pre-existing conditions, these parents do not have to worry about whether their son can access coverage when he is no longer on their plan.

If the ACA were repealed:

-

This couple would face significant financial burdens in caring for their son. Given the significant costs associated with caring for complex heart defects, they could very quickly reach the lifetime limit on their plan, in addition to the significant out-of-pocket costs they would incur.

-

They would then be forced to either find a new job that provided coverage without a lifetime limit or find a way to pay for the costs of their son’s care on their own.

-

In addition, their employer’s plan would not necessarily need to cover their son until age 26, meaning that, once he is older, he would need to find an alternative source of coverage to provide for his ongoing care.

-

And, because of discrimination against individuals with pre-existing conditions, he may not ever be able to obtain coverage again.

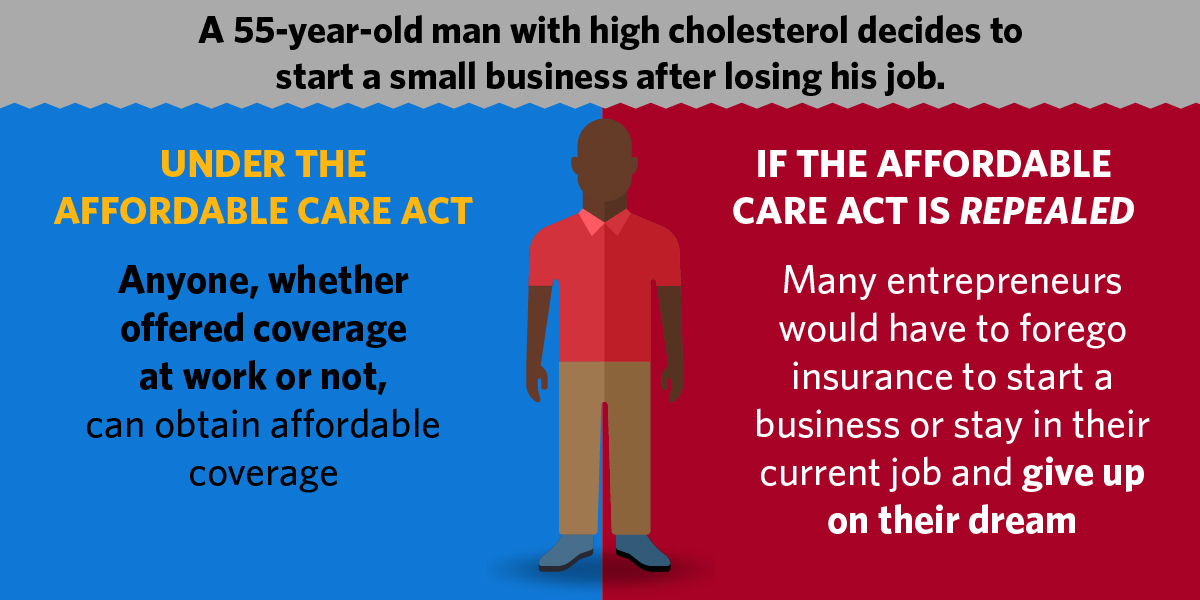

A 55-year-old man with a history of high cholesterol loses his job. He decides to start his own small business. The ACA helps him find affordable health coverage even though he has a pre-existing condition. And, it makes it easier for him to provide health insurance to his employees as his small business grows by providing tax credits and ensuring premium dollars go to providing care rather than padding insurers’ profits.

More on how the ACA helps:

-

He is able to obtain coverage on the Marketplace after losing his job, meaning that he is free to start his own business rather than work for a large business just to keep his health coverage.

-

He cannot be discriminated against because of his high cholesterol, which affects over 73 million Americans.

-

Moreover, if his high cholesterol leads to a heart attack or other significant health event, his insurer cannot cancel his plan over a technicality regarding the form he filled out when signing up for coverage, such as forgetting to report that he had chicken pox as a child.

-

All individual market plans now cover prescription drugs, so he can obtain medication to help address his high cholesterol and prevent future health problems.

-

As his business expands, he can use the Marketplace for small businesses to easily compare and shop for plans for his employees and offer them a range of options that work for his business and for them.

-

An ACA provision requires that plans spend at least 80 percent of premiums on covering the cost of care or making quality improvements, to ensure he is getting the best value for his dollar. Thanks to this provision, nearly $2.8 billion in rebates have been paid to Americans from 2011-2015.

-

And, because of the ACA, his small business qualifies for a tax credit worth up to 50 percent of the cost he pays for his employees’ coverage.

If the ACA were repealed:

-

This man would have significant trouble finding coverage.

-

To start his own business, he would likely have to forgo insurance, as his pre-existing condition would make it difficult to find an affordable plan.

-

He would be in danger of his insurer canceling his plan the moment he had a significant health condition, and his plan might not cover the prescription drugs he needs to treat his high cholesterol, as was the case for almost one in ten people in the individual market prior to the ACA.

-

If he were able to start his own business, he could find it difficult to provide health care for his employees, particularly given the lack of a small business tax credit to help offset costs.

-

His employees, now forced to find insurance on their own without ACA consume protections, would face the same sorts of issues he did in finding coverage. They may also prefer to work for a company that offers health benefits.

-

And his insurance company could use less of his premium dollars to provide care, instead using them to pay for marketing or company profits.

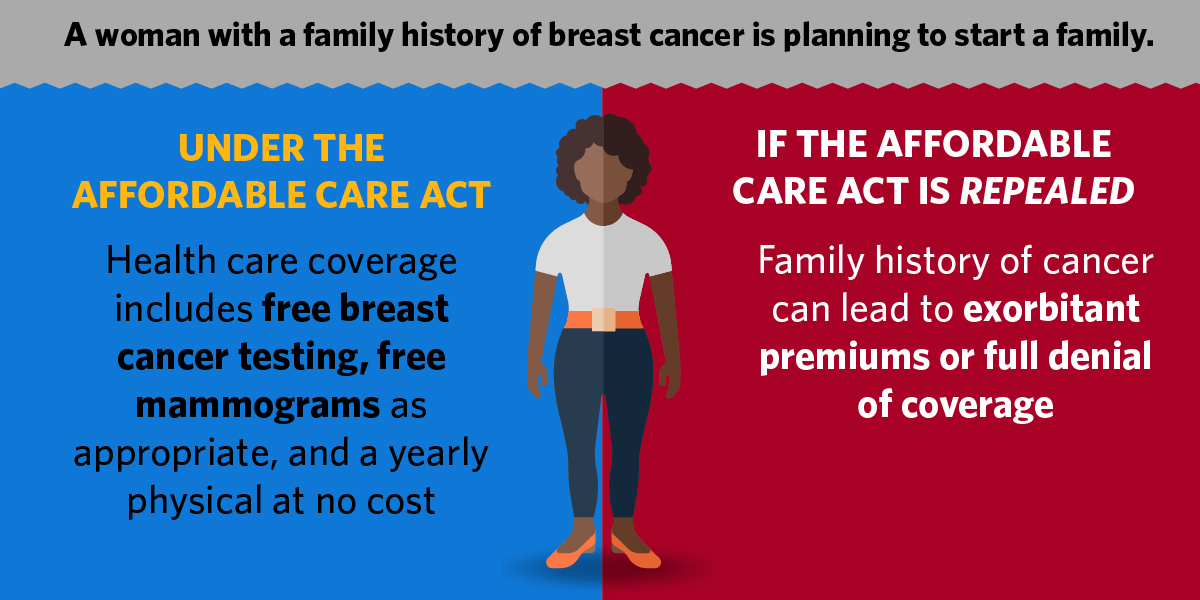

A newly married woman with a family history of breast cancer is seeking a new individual market insurance plan. Thanks to the ACA, she can find affordable coverage despite her family history of break cancer. Her coverage will provide free preventive services to help her manage her risk of breast cancer. She is also considering starting a family. Her coverage will also cover important preventive services for women who may become pregnant and provide her with contraception, both free of charge.

More on how the ACA helps:

-

She does not need to worry that her family history of breast cancer will be treated as a pre-existing condition that prevents her from getting an offer of coverage, being charged more for coverage, or having cancer treatment excluded from coverage.

-

Her coverage will include free breast cancer genetic test counseling and, as she gets older, free mammograms as appropriate.

-

And any coverage that she receives will provide a range of free preventive screenings that are important for women who may become pregnant.

-

It will also cover a yearly physical at no cost.

-

In addition, she will be able to obtain birth control free of charge, and her plan will be required to cover care provided at community health centers and family planning clinics.

If the ACA were repealed:

-

This woman could face significant problems finding coverage and making family planning decisions that are right for her.

-

She could be excluded from coverage or charged exorbitant rates because of her family history.

-

If she were able to find coverage, it would likely not provide preventive services free of charge, making it more difficult to manage her risk of breast cancer.

-

She would find it more difficult to engage in effective family planning. Screenings could be costly, and she would have to pay for contraceptive coverage as well.

-

She would not be guaranteed an annual well woman’s visit without out of pocket costs.

-

And there would be no guarantee that her plan would cover care at nearby community health centers or family planning clinics, which could require her to travel significant distances to get needed care at an affordable cost.

Jeanne Lambrew is Deputy Assistant to the President for Health Policy.