Five years after the financial crisis

In the early hours of September 15, 2008 Lehman Brothers announced it would file for Chapter 11 bankruptcy protection, setting off shock waves through the global economy that had devastating implications for families and businesses. In the months before the President took office, the economy was shrinking at a rate of more than 8 percent and we were losing 800,000 jobs a month.

There's no diminishing the severity of the challenge we've overcome together, and we’ve got a lot more work to do to rebuild an economy where everyone who works hard has a chance to get ahead. Learn more about how you can help to build on this progress. Or download the report: The Financial Crisis: Five Years Later.

But five years after Lehman Brothers' bankruptcy, we want to help everyone get the context and see the full picture. To mark the anniversary, we've asked senior staff from across the Obama administration to sit down and talk about the moments when key decisions were made — the factors they weighed, the results of the actions that President Obama took. Check out a behind-the-scenes look of the decision-making process that you won't find anywhere else.

Saving the American Auto Industry

Deputy Director of the Office of Management and Budget

Prior to this role as the Deputy Director of the Office of Management and Budget (OMB), Brian Deese served as Deputy Director of the National Economic Council (NEC), charged with coordinating policy development on several Administration economic priorities.

Five Years Ago

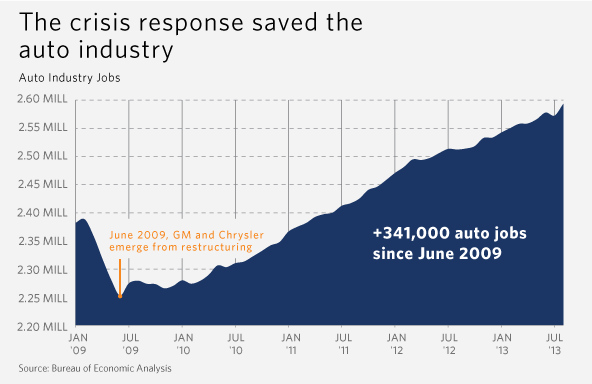

- GM and Chrysler near bankruptcy - Auto sales down 40 percent - 1 million jobs at riskAdministrative Actions

- Challenged GM and Chrysler to restructure - Launched “Cash for Clunkers” to boost demandWhere We Are Today

- Ford, Chrysler and GM are profitable and sales are growing - More cars and trucks were exported in 2012 than ever beforeHealing the Housing Market

U.S. Secretary of Housing and Urban Development

Shaun Donovan is the 15th United States Secretary for Housing and Urban Development (HUD), holding the role since January 2009. He has devoted his career to ensuring access to safe, decent, and affordable housing.

Five Years Ago

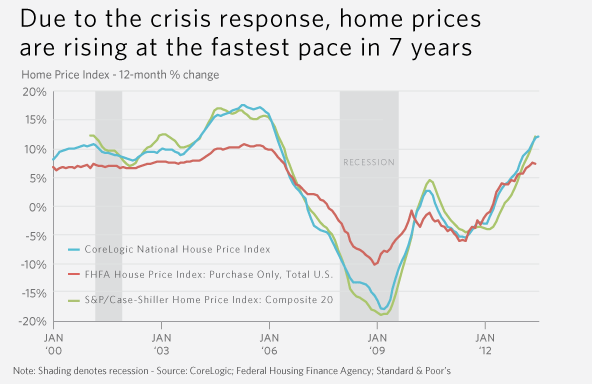

- Home prices down by 19% from a year earlier - 10 million borrowers underwater - Home sales near all-time lowsAdministrative Actions

- Helped millions modify home loans to avoid foreclosure - Expanded mortgage refinancing for underwater borrowers - Created the CFPB to make buying a home simpler and saferWhere We Are Today

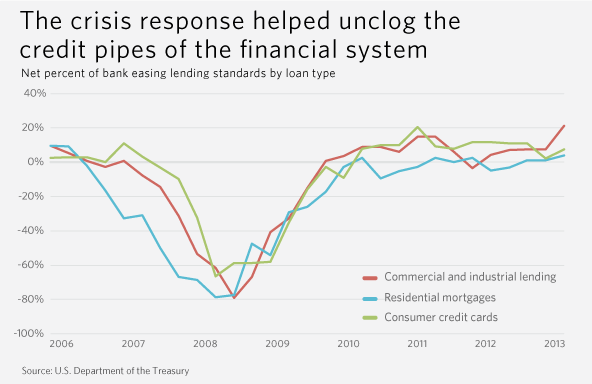

- Home prices rising at the fastest pace in 7 years - Home sales are up 47% - Homeowners’ equity is up $2.8 trillion since 2009 lowStabilizing the Financial System

Director of the National Economic Council and Assistant to the President for Economic Policy

Upon his appointment in January 2011, Mr. Sperling became the first person to serve as NEC Director and principal economic policy advisor for two presidents: first under President Clinton and now under President Obama.

Five Years Ago

- American economy on the brink of collapse - Banks and financial institutions failing - Auto companies struggling - Housing market in free fallAdministrative Actions

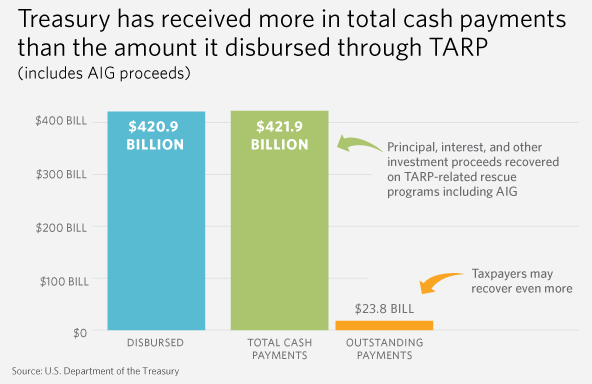

- Signed the Recovery Act - Stabilized the financial system - Used TARP funds to help homeowners and restructure the auto industryWhere We Are Today

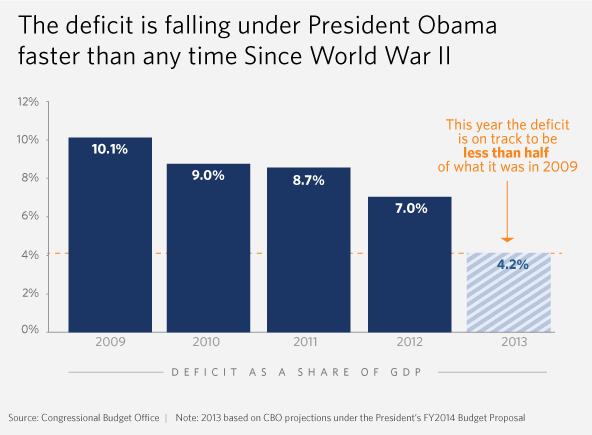

- Government expected to profit from financial crisis response - More confidence in the banking system, less taxpayer risk - Auto industry is growing, housing market is healingReducing the Deficit

Director of the Office of Management and Budget

Sylvia Mathews Burwell was confirmed by the Senate in 2013 as the Director of the Office of Management and Budget (OMB). During the Clinton Administration, she served as Deputy Director of OMB, Deputy Chief of Staff to the President, Chief of Staff to the Secretary of the Treasury, and Staff Director of the National Economic Council.

Five Years Ago

- President Obama inherits over $1 trillion deficit from the previous administrationAdministrative Actions

- Cut spending by $1.4 trillion - Reduced the deficit by more than $2.5 trillionWhere We Are Today

- Domestic discretionary spending is on track to be at its lowest level as a share of the economy since the Eisenhower eraProtecting Consumers

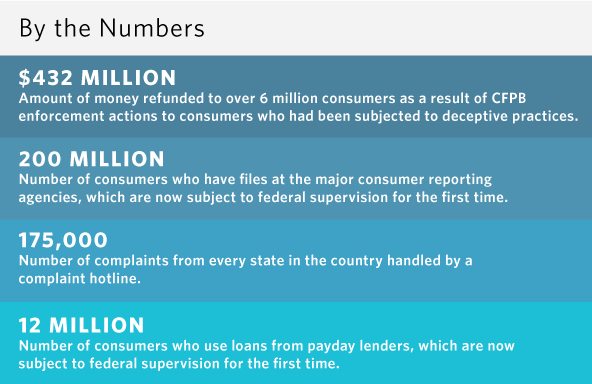

Deputy Press Secretary

Amy Brundage currently serves as the Deputy Press Secretary for the Economy and previously held the Regional Communications Director position in the Obama Administration.

Follow on Twitter

@Brundage44

Five Years Ago

- Predatory lending misled borrowers to take on unaffordable mortgages - Little regulation for consumer financial industries like payday lenders and debt collectors - No agency whose sole job was to protect middle-class consumersAdministrative Actions

- Established the Consumer Financial Protection Bureau - Held banks accountable for predatory actionWhere We Are Today

- Consumer reporting agencies, debt collecting agencies and payday lenders subject to federal regulations - Companies refunded 6 million customers $400 million for using deceptive marketing or charging unreasonable feesSupporting Business

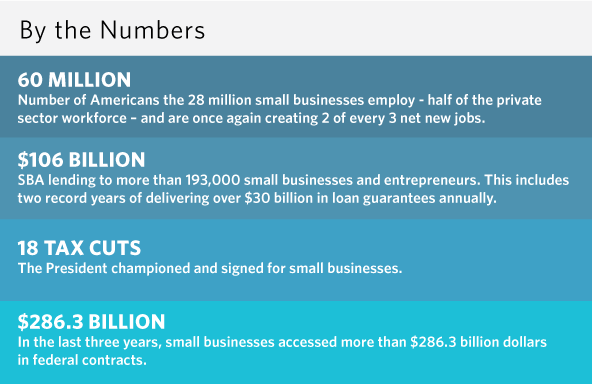

U.S. Secretary of Commerce

Penny Pritzker is the 38th Secretary of Commerce, since June 2013. For the previous two years, Ms. Pritzker served the Obama Administration as a member of the President's Economic Recovery Advisory Board which formulated and evaluated economic policy.

Five Years Ago

- Dramatically reduced credit available for small businesses - More small businesses declaring bankruptcyAdministrative Actions

- Ensured access to business lending through SBA - Cut taxes and signed legislation to support small business growthWhere We Are Torday

- More available capital and lending for small business - More small businesses approved for loansReforming Wall Street

Chairman of the Council of Economic Advisers

Prior to Jason Furman's role as the Chairman of the Council of Economic Advisers (CEA), he served as Assistant to the President for Economic Policy and the Principal Deputy Director of the National Economic Council. Previously, he served at the CEA and National Economic Council (NEC) under President Clinton.