The Final State of the Union

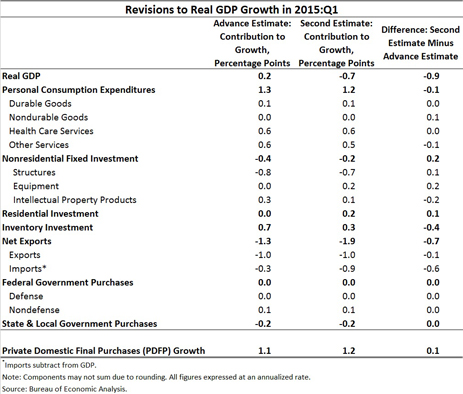

Today’s downward revision to GDP growth was entirely accounted for by revisions to inventory investment and net exports, with other changes being small and neutral on balance. The first-quarter slowdown was the result of harsh winter weather, tepid foreign demand, and consumers saving the windfall from lower oil prices. The combination of personal consumption and fixed investment, the most stable components of GDP, has grown 3.4 percent over the past four quarters. This solid long-term economic trend complements the robust pace of job growth and unemployment reduction over the last year. The President is committed to further strengthening these positive trends by opening our exports to new markets with new high-standards free trade agreements that create opportunities for the middle class, expanding investments in infrastructure, and ensuring the sequester does not return in the next fiscal year as outlined in the President’s FY2016 Budget.

FIVE KEY POINTS IN TODAY’S REPORT FROM THE BUREAU OF ECONOMIC ANALYSIS

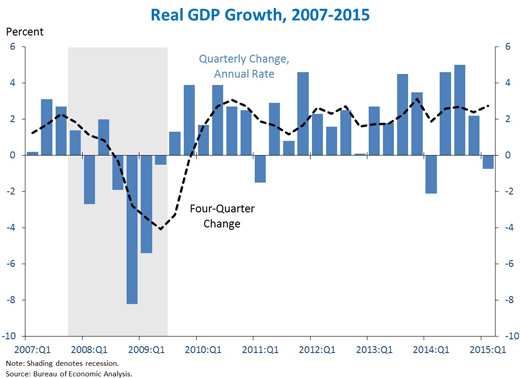

1. Real gross domestic product (GDP) fell 0.7 percent at an annual rate in the first quarter of 2015, according to the second estimate from the Bureau of Economic Analysis. The decline follows an increase of 3.6 percent at an annual rate during the second half of 2014. First-quarter growth was likely affected by a number of factors including especially harsh winter weather in the first quarter (see point 3) and a spike in personal saving (see point 4). A decline in the trade balance was another major contributor, partially reflecting the continued drag on U.S. exports from the slowdown in foreign growth. Indeed, net exports subtracted nearly 2 full percentage points from quarterly GDP growth. Structures investment subtracted about 0.7 percentage point from GDP, likely reflecting reduced oil mining in the wake of last year’s decline in oil prices.

Real private domestic final purchases (PDFP) — the sum of consumption and fixed investment — rose 1.2 percent at an annual rate in the first quarter, a faster pace than overall GDP. Real PDFP growth is generally a more stable and forward-looking indicator than real GDP, as it excludes volatile components like inventories, net exports, and government spending. PDFP is a better predictor of next-quarter GDP than GDP itself. The year-over-year growth rate of PDFP rose this quarter to 3.4 percent.

2. The entire downward revision to first-quarter GDP can be accounted for by downward revisions to two especially volatile components of economic output: inventory investment and net exports. Inventories and net exports subtracted a combined 1.1 percentage points from annualized GDP growth relative to the Bureau of Economic Analysis’ first estimate. At the same time, business investment added 0.2 percentage point more than originally estimated. Other small revisions to the contributions of personal consumption expenditures and residential investment offset one another.

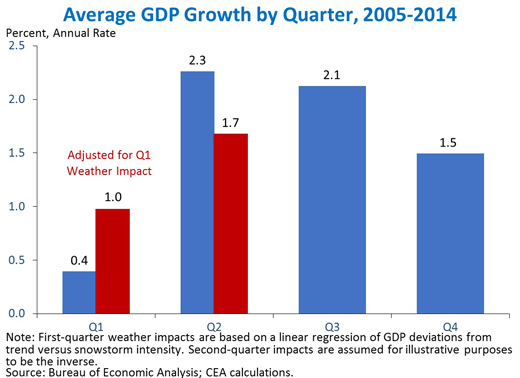

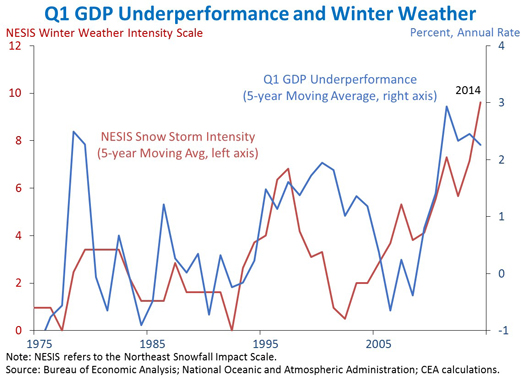

3. Over the past decade, first-quarter GDP growth has averaged a considerably slower pace than the other three quarters. Economists have debated whether this gap reflects a problem with the algorithms used to seasonally adjust GDP data (“residual seasonality”), especially harsh winter weather in recent years, or noise. The seasonal adjustment process should remove the growth effects of “normal” winter weather, but particularly harsh winters will still reduce seasonally adjusted output. And weather in the first quarter was especially harsh: Q1 was only the fourth quarter in 60 years on record with three or more snowstorms sufficiently severe to be rated by the National Climatic Data Center’s Northeast Snowfall Impact Scale (NESIS). The historical relationship between weather and first-quarter growth suggests that weather may have reduced annualized growth by about a full percentage point this quarter, and by about 0.6 percentage point on average over the past decade. That effect accounts for much, but not all, of first-quarter underperformance since 2005.

The debate so far over the cause of first-quarter underperformance has tended to treat residual seasonality and weather effects as analytically distinct explanations. However, to the extent that worsening winter weather is part of a long-term trend rather than a random occurrence, changing weather patterns may be related to residual seasonality. A seasonal adjustment algorithm should adjust for effects of normal weather within a particular quarter—and to the extent that global climate change leads to a new “normal” for weather, seasonal adjustments will eventually catch up. Indeed, first-quarter underperformance (defined as the difference between GDP growth in the first-quarter and the rest of the year) has tended to increase over the past ten years, in parallel with intensifying winter weather.

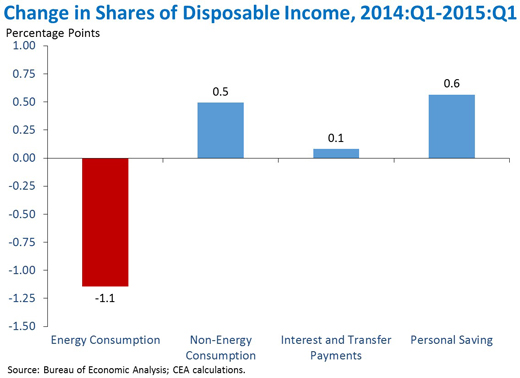

4. Consumers have so far saved most of their windfall gains from last year’s energy price decline. Since June, national average gasoline prices have fallen more than $1 per gallon, providing the equivalent of about a $700 tax cut per household. Looking over the past year, energy consumption as a share of disposable personal income has declined by 1.1 percentage points, leaving more space in consumer checkbooks to save and spend. To date, however, households appear to have put most of those gains in the bank, as the personal saving rate has risen by 0.6 percentage point over the past four quarters. Just over the last quarter, the personal saving rate rose 0.8 percentage point—an unusually large increase that is at the 88th percentile of historic increases.

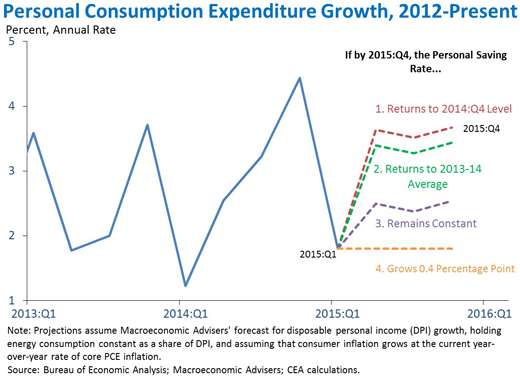

Historically, the personal saving rate has tended to revert to its short-term mean; temporary spikes like this one do not usually persist. If the saving rate returns to normal levels with continued growth in real disposable personal income and no major resurgence in gasoline prices, personal consumption growth is likely to increase. If the saving rate returns to its previous level by the end of 2015, consumer spending would grow at a nearly 4 percent annual rate for the final three quarters of the year. If the saving rate remains constant at the new higher level, consumer spending growth would also pick up somewhat to a 2.5 percent annual rate for the final three quarters of the year. Given the current forecasts for growth in disposable personal income, the saving rate would have to rise by another 0.4 percentage point by the end of the year to continue the 1.8 percentage point annualized growth rate in Q1. All told, the difference between a mean reverting saving rate and a rising saving rate is about 0.8 percentage point for GDP growth for the four quarters of 2015.

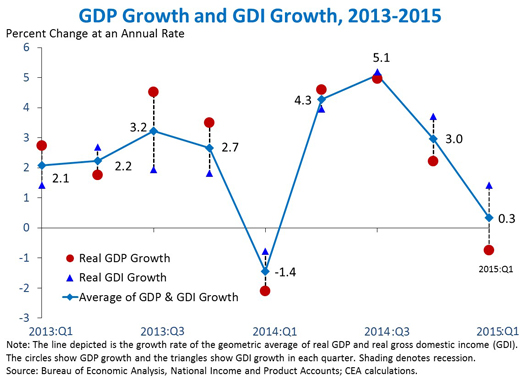

5. Gross domestic income (GDI)—an alternate indicator of economic output that would equal GDP absent measurement error—grew an estimated 1.4 percent at an annual rate in the first quarter, faster than estimated GDP. Over the last four quarters, real GDI grew 3.6 percent, as compared with the 2.7 percent growth in real GDP over that period. GDP gauges overall activity by measuring the final expenditures of households, businesses, governments, and trading partners in a given time period, while GDI measures the incomes generated during that production process. If we had perfect information, the two measures would equal one another: they are conceptually identical as a measure of economic activity. But because the data underlying each are gathered from different sources, they often differ substantially in practice due to measurement error. This quarter, although GDP fell at a 0.7 percent annualized rate, GDI rose at a 1.4 percent annualized rate. This 2.1 percentage point gap reflects the inherent uncertainty underlying measures of aggregate output, and underscores the importance of focusing on multiple data sources and longer term trends. Some economists track the average of the two measures as a more stable gauge of activity, a measure BEA will start reporting in July. The average of GDP and GDI rose 0.3 percent at an annual rate in the first quarter. While combining information from GDP and GDI can help reduce measurement error about what actually happened in the current period, PDFP (see point 1) may provide a better indication of growth in future periods because it omits noisy economic developments.

As the Administration stresses every quarter, GDP figures can be volatile and are subject to substantial revision. Therefore, it is important not to read too much into any one single report, and it is informative to consider each report in the context of other data that are becoming available.