Council of Economic Advisers Blog

On the December Jobs Numbers

Posted by on January 8, 2010 at 9:37 AM ESTToday’s employment report, though a setback from November, is consistent with the gradual labor market stabilization we have been seeing over the last several months.

Payroll employment declined 85,000 in December. To put this number in perspective, employment declined 139,000 in September and 127,000 in October. So, in a broad sense the trend toward moderating job loss is continuing. This trend is particularly obvious in the quarterly pattern: average monthly job loss was 691,000 in the first quarter of 2009, 428,000 in the second quarter, 199,000 in the third quarter, and 69,000 in the fourth quarter.Revised data now show that employment increased 4,000 in November. This is obviously welcome news and the first employment increase in 23 months. Compared with the unexpectedly good report for November, December’s job loss is a slight setback. Two industries where employment declined significantly were construction (-53,000) and wholesale and retail trade (-28,400). One continuing sign of labor market healing was that temporary help services, which is often a leading indicator of labor demand, added 46,500 jobs in December. Both the work week and aggregate hours remained stable, maintaining the significant improvement that occurred in November.

The unemployment rate remained at 10.0 percent in December. This level reflected a proportional decline in the number of people unemployed and the number of people in the labor force. The unemployment rate remains unacceptably high, which underscores the need for responsible actions to jumpstart private-sector job creation.

As the President has said for a year, the road to recovery will not be a straight line. The monthly employment and unemployment numbers are volatile and subject to substantial revision. Therefore, it is important not to read too much into any one monthly report, positive or negative. It is essential that we continue our efforts to move in the right direction and replace job losses with robust job gains.

Christina Romer is Chair of the Council of Economic Advisers

Learn more about EconomyOn Today's GDP Numbers

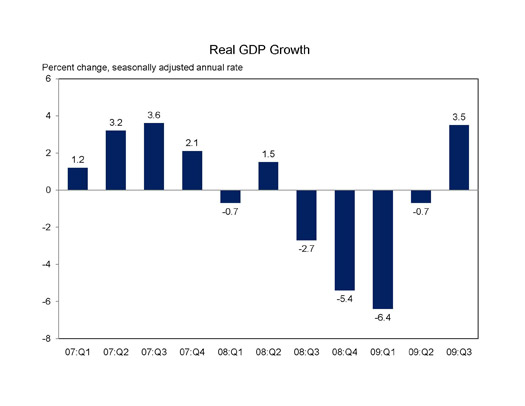

Posted by on October 29, 2009 at 8:30 AM ESTData released today by the Commerce Department show that real GDP grew at an annual rate of 3.5 percent in the third quarter of the year. This is in stark contrast to the decline of 6.4 percent annual rate just two quarters ago. Indeed, the two-quarter swing in the rate of growth of 9.9 percentage points was the largest since 1980. Analysis by both the Council of Economic Advisers and a wide range of private and public-sector forecasters indicates that the American Recovery and Reinvestment Act of 2009 contributed between 3 and 4 percentage points to real GDP growth in the third quarter. This suggests that in the absence of the Recovery Act, real GDP would have risen little, if at all, this past quarter.

After four consecutive quarters of decline, positive GDP growth is an encouraging sign that the U.S. economy is moving in the right direction. However, this welcome milestone is just another step, and we still have a long road to travel until the economy is fully recovered. The turnaround in crucial labor market indicators, such as employment and the unemployment rate, typically occurs after the turnaround in GDP. And it will take sustained, robust GDP growth to bring the unemployment rate down substantially. Such a decline in unemployment is, of course, what we are all working to achieve.

Christina Romer is Chair of the Council of Economic Advisers

Learn more about Economy

White House Blogs

- The White House Blog

- Middle Class Task Force

- Council of Economic Advisers

- Council on Environmental Quality

- Council on Women and Girls

- Office of Intergovernmental Affairs

- Office of Management and Budget

- Office of Public Engagement

- Office of Science & Tech Policy

- Office of Urban Affairs

- Open Government

- Faith and Neighborhood Partnerships

- Social Innovation and Civic Participation

- US Trade Representative

- Office National Drug Control Policy

categories

- AIDS Policy

- Alaska

- Blueprint for an America Built to Last

- Budget

- Civil Rights

- Defense

- Disabilities

- Economy

- Education

- Energy and Environment

- Equal Pay

- Ethics

- Faith Based

- Fiscal Responsibility

- Foreign Policy

- Grab Bag

- Health Care

- Homeland Security

- Immigration

- Innovation Fellows

- Inside the White House

- Middle Class Security

- Open Government

- Poverty

- Rural

- Seniors and Social Security

- Service

- Social Innovation

- State of the Union

- Taxes

- Technology

- Urban Policy

- Veterans

- Violence Prevention

- White House Internships

- Women

- Working Families

- Additional Issues