The Final State of the Union

First-quarter economic growth was revised up 0.3 percentage point to 1.1 percent at an annual rate. Strong growth in residential investment boosted real GDP growth, but weakness in business investment—exacerbated by weak foreign demand and low oil prices—weighed on growth. Going forward, increased uncertainty, including uncertainty regarding the consequences of British voters' decision last week to leave the European Union, underscores the importance of proactive policy steps to strengthen the U.S. economy. The President will continue to take steps to strengthen economic growth and boost living standards, including promoting greater competition across the economy; supporting innovation; and calling on Congress to support investments in infrastructure and job training and to pass high-standards free trade agreements like the Trans-Pacific Partnership.

FIVE KEY POINTS IN TODAY'S REPORT FROM THE BUREAU OF ECONOMIC ANALYSIS (BEA)

1. Real Gross Domestic Product (GDP) grew 1.1 percent at an annual rate in the first quarter of 2016, according to BEA’s third estimate. In the first quarter, GDP grew faster than previously estimated, but growth remained modestly slower than the 1.4-percent rate in the fourth quarter of 2015. GDP growth was supported by strength in residential investment, which increased 15.6 percent. Consumer spending grew 1.5 percent, a moderate pace but below its rate over the prior four quarters. Business investment contracted 4.5 percent in the first quarter, reflecting ongoing declines in oil-related structures investment as well as a decline in equipment investment. Slowing global demand continues to remain a key headwind to output growth, though real exports increased 0.3 percent in the first quarter.

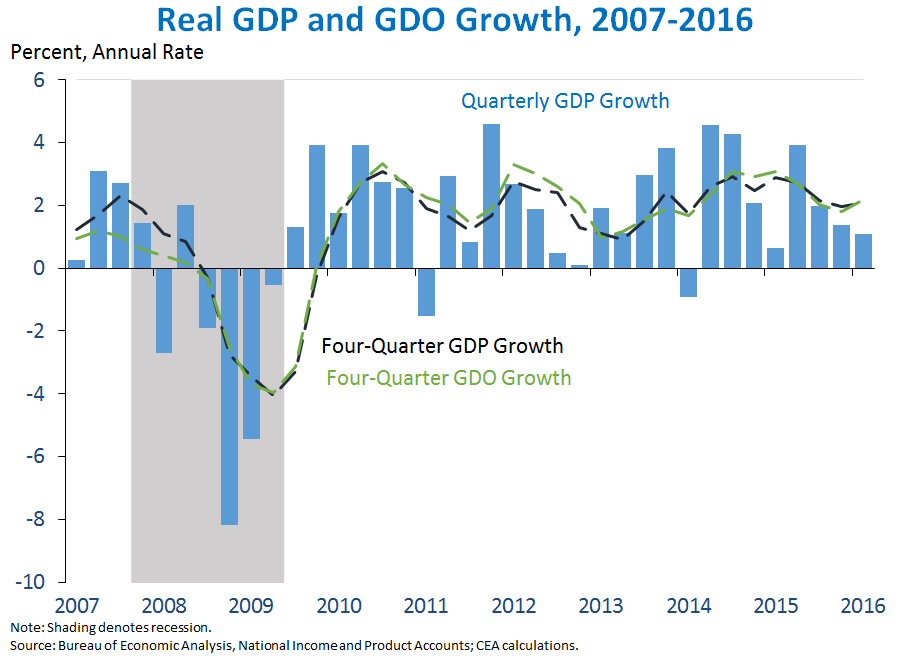

However, other indicators provide a stronger picture of first-quarter growth. Real Gross Domestic Income (GDI)—an alternative measure of output—grew 2.9 percent at an annual rate in the first quarter, well above the increase in GDP. (In theory, these two measures should be equal, but in practice often differ because they use different data sources and methods.) The average of GDP and GDI, which CEA refers to as Gross Domestic Output (GDO), increased 2.0 percent at an annual rate in the first quarter. CEA research suggests that GDO is potentially a better measure of economic activity than GDP (though not typically stronger or weaker).

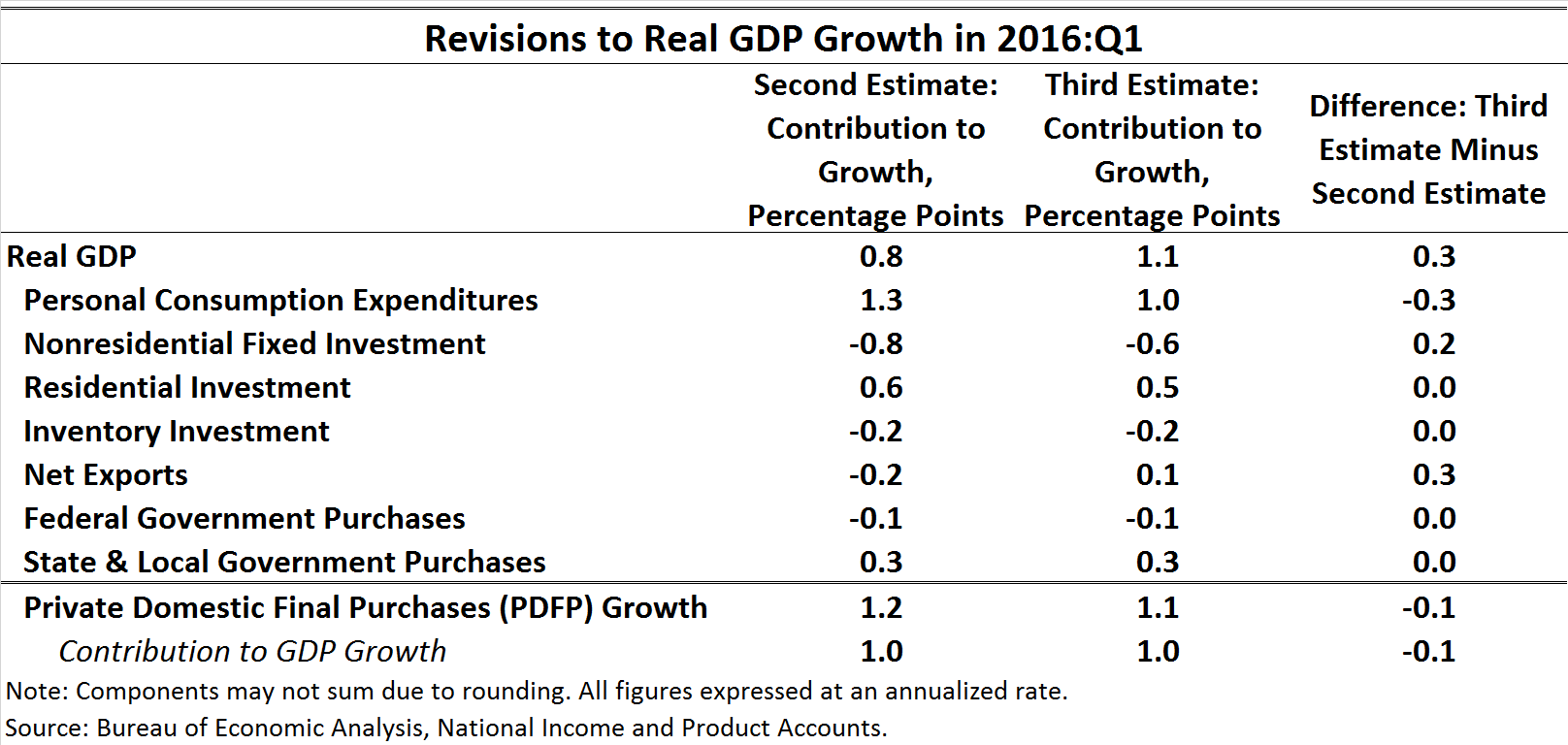

2. First-quarter GDP growth was revised up 0.3 percentage point at an annual rate. The upward revision to GDP growth was largely accounted for by upward revisions to exports and investment in intellectual property products, with a partially offsetting downward revision in consumer spending on services (reflecting the incorporation of new data from the Census Bureau’s Quarterly Services Survey).

In today’s release, BEA also revised up its estimate of real GDI growth in the first quarter from 2.2 percent to 2.9 percent due to an upward revision to corporate profits. As a result, first-quarter GDO growth was revised up to 2.0 percent, a stronger pace than the previously reported 1.5 percent.

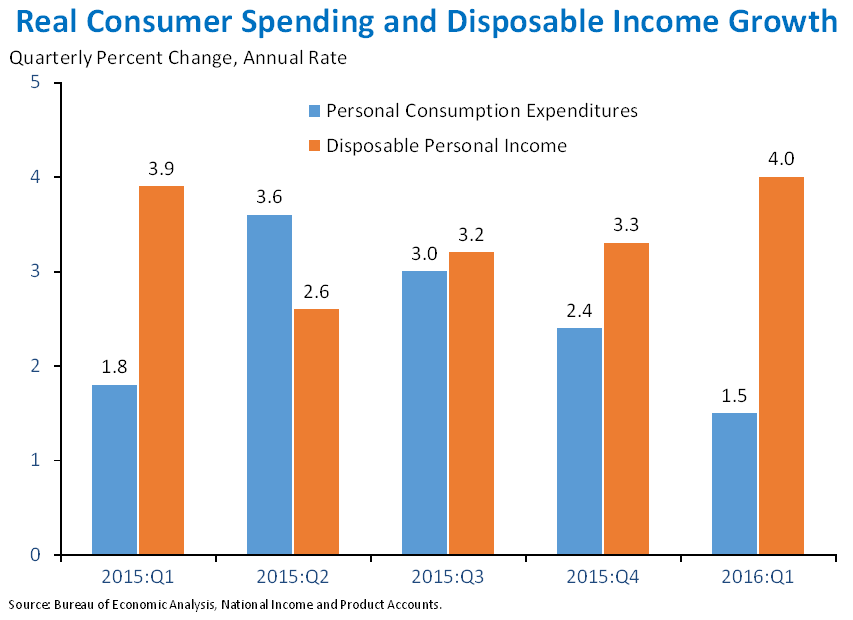

3. While growth in consumer spending slowed somewhat in the first quarter, monthly data through May point to a pickup in the second quarter. Consumer spending increased 1.5 percent at an annual rate in the first quarter, below its 2.7-percent pace over the previous four quarters. The first-quarter slowdown was largely driven by a decline in durable goods spending. However, measures of consumer spending that are reported on a monthly basis—including retail sales and motor vehicle sales—rebounded in April and were solid in May, consistent with a pickup in growth in the second quarter. In addition, growth in real disposable income has outpaced growth in real consumer spending in recent quarters, especially in the first quarter of 2016, providing support in future quarters for further growth in consumer spending.

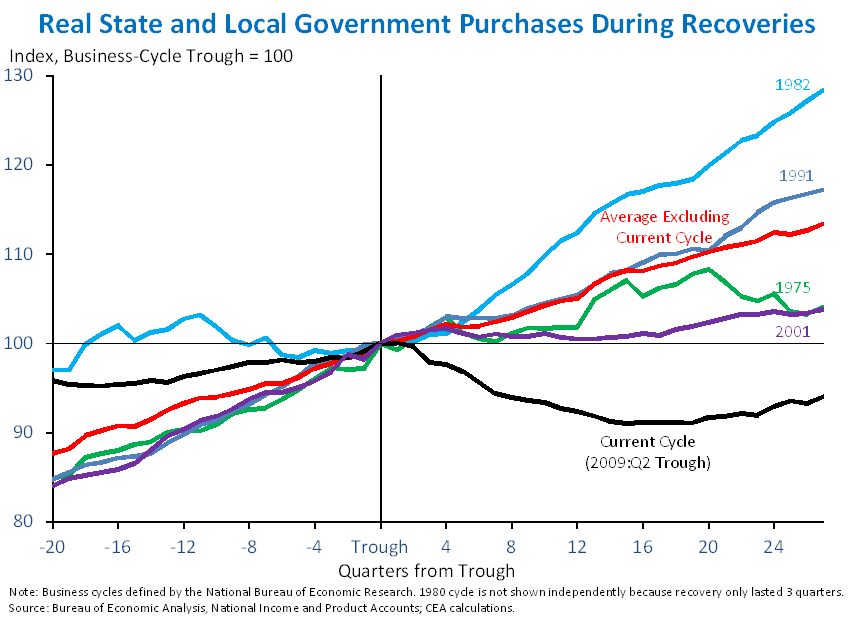

4. Real State and local government purchases—which had faced challenges earlier in the recovery—increased 3.2 percent at an annual rate in the first quarter. Contraction in State and local government purchases amid budgetary cuts was a meaningful drag on GDP growth earlier in the current recovery, particularly when compared to earlier business cycles. If State and local government purchases had increased at the average rate of the prior four recoveries, real GDP growth would have been 0.4 percentage point faster per year in the first five years of the current recovery. State and local government purchases remain 6 percent below their level at the business-cycle trough, compared with an average 13-percent increase at this point during the four previous business cycles. However, since mid-2014 the State and local government sector has generally added modestly to GDP growth, contributing 0.3 percentage point to growth in the first quarter of 2016.

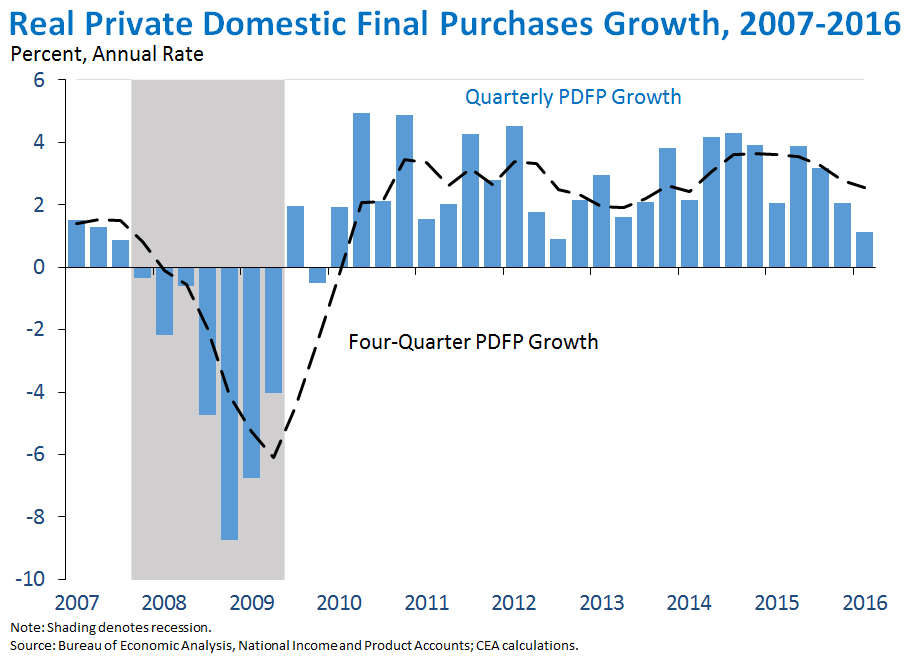

5. Real private domestic final purchases (PDFP)—the sum of consumption and fixed investment—rose 1.1 percent at an annual rate in the first quarter, a slower pace than in recent quarters. PDFP—which excludes noisier components of GDP like net exports and inventory investment, as well as government spending—is generally a more reliable indicator of next-quarter GDP growth than current GDP. In recent quarters, weaker demand abroad has dampened business investment, and low oil prices have weighed on energy-related investment, both of which have led to slower PDFP growth. Overall, PDFP rose 2.5 percent over the past four quarters, above the 2.1-percent growth in GDP over the same period.

As the Administration stresses every quarter, GDP figures can be volatile and are subject to substantial revision. Therefore, it is important not to read too much into any single report, and it is informative to consider each report in the context of other data as they become available.